As discussed in the first installment of this five-part series, the increasing population affected by kidney diseases such as chronic kidney disease (CKD) and end-stage renal disease (ESRD), as well as the increase in the healthcare spending on kidney diseases, has led to growth in dialysis centers.1 This second installment in the five-part series will review the competitive environment of dialysis centers.

Demand for Dialysis Services

Demand for dialysis services is likely to increase significantly in the near future, primarily as a result of: (1) the increasing life expectancy for ESRD patients; (2) the disease-specific entitlement to Medicare coverage for ESRD patients, regardless of age; and, (3) the changing demographic trends in the U.S.2

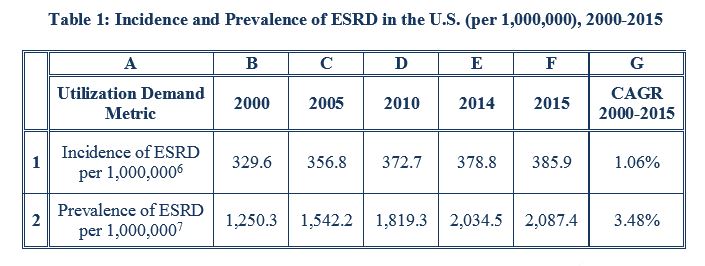

Statistics related to the incidence and prevalence of ESRD indicate the potential for increased demand for dialysis services. Notably, the incidence, i.e., the occurrence of new instances, of ESRD patients nationally per year has been rising since 2011.3 The improvements in life expectancy of ESRD patients receiving dialysis treatments has led to a similar growth in the prevalence, i.e., the total number of affected persons, of ESRD, as the unadjusted death rate from ESRD in the U.S. declined 20% from 2003 to 2012.4 This increase in the life expectancy of ESRD patients, coupled with stable incidence rates for ESRD, is driving increased prevalence of ESRD, which may drive demand for dialysis services.5

Table 1, below, details trends in the incidence and prevalence of ESRD in the U.S. from 2000 to 2015.

From 2015 to 2016, the number of Medicare beneficiaries receiving dialysis treatments increased by one percent, while the number of dialysis treatments provided to Medicare beneficiaries, increased by approximately three percent.6 Although Medicare dialysis beneficiaries are generally younger than most Medicare beneficiaries (in 2016, over 50% of all Medicare ESRD beneficiaries receiving dialysis treatments were under the age of 65),7 improved life expectancy among ESRD patients may increase the number of dialysis beneficiaries over the age of 65, a population cohort disproportionately driving healthcare expenditures due, in part, to the sufferance of chronic conditions at rates higher than the average population.8 With this cohort expected to constitute an increasing proportion of the U.S. population, meeting the needs of aging dialysis beneficiaries managing multiple comorbidities may influence dialysis care models in the future.

Supply of Dialysis Centers

As of 2018, Centers for Medicare & Medicaid Services (CMS) certified 6,825 dialysis facilities across the U.S.9 A significant majority of dialysis facilities are freestanding, for-profit facilities; in 2016, freestanding facilities provided 94% of dialysis treatments to Medicare ESRD beneficiaries, while over the same period, for-profit facilities provided 90% of dialysis treatments to this cohort.10

Consolidation among dialysis providers has led to high levels of market concentration in this industry.11 In 2014, DaVita HealthCare Partners (DaVita) and Fresenius Medical Care (Fresenius), the country’s two largest dialysis organizations, treated 69% of all patients in 65% of all dialysis facilities in the U.S.12

According to a 2007 article in the Journal of the American Society of Nephrology, industry consolidation among dialysis centers may have potential advantages, e.g., certain economies of scale; technical efficiencies; improved information and tracking systems; access to capital; and, vertical integration opportunities.13 Industry consolidation also has the potential to offer certain clinical advantages, including the potential for improved compliance with process and protocols; accountability; standardization of care across a large system; and, integrated information and reporting systems.14 Such horizontal integration may impact the local competitive environment for dialysis facilities, as the scope of treatment options and services provided may influence the decisions of the patient and their physician as to the appropriate facility to receive dialysis treatments.15

Competition with Other Providers of ESRD Treatment

The varied forms of treatment for ESRD, as well as the varied sites of service for dialysis care, create various competitive pressures for dialysis centers. Regarding the various forms of treatment for ESRD, dialysis centers face competition from providers of kidney transplantation services, as the patient’s receipt of a new kidney would eliminate the need to receive dialysis care.16 Further, receipt of a kidney transplant “is associated with a substantial survival benefit relative to chronic dialysis,” making access to kidney transplants a “prominent public health priority.”17 With the increasing strength of this competitive force nationally, the impact of kidney transplants on the operations of dialysis centers in the U.S. may also be increasing. After stagnating growth from 2006 to 2012,18 the number of U.S. kidney transplants increased from 16,896 in 2013 to 19,849 in 2017, a compound annual growth rate (CAGR) of approximately 4.11% over the time period.19

Regarding the varied sites of service for dialysis care, dialysis centers face competition from hospital providers of dialysis treatments. In 2016, hospital-based dialysis centers accounted for 6% of treatments to Medicare ESRD beneficiaries, 5% of all dialysis stations, and 6% of all CMS-certified dialysis facilities, with the remaining percentages held by freestanding dialysis centers.20 While patients with additional health issues beyond ESRD may find a benefit in receiving dialysis care in a hospital setting, companies providing outpatient dialysis care may limit this competitive pressure by contracting with the hospital to manage its dialysis clinic.21

Competing with other providers of dialysis care (e.g., hospitals) and the rising number of dialysis centers (i.e., potential competitors) pose a challenge to dialysis centers, but the aging “baby boomer” population and growing prevalence of ESRD are likely to create more opportunities for these dialysis centers to exploit.

For more information, see the first installment of this five part series: “Valuation of Dialysis Centers: Introduction” Health Capital Consultants, Vol. 11, Issue 10 (October 2018), https://www.healthcapital.com/hcc/newsletter/10_18/PDF/DIALYSIS.pdf (Accessed 10/23/18).

“Chapter 1: Incidence, Prevalence, Patient Characteristics, and Treatment Modalities” in “2017 USRDS Annual Data Report: Volume 2 – ESRD in the United States” United States Renal Data System, 2017, https://www.usrds.org/2017/view/v2_01.aspx (Accessed 10/23/18).

“Global Challenges Posed by the Growth of End-Stage Renal Disease” By James B. Wetmore and Allan J. Collins, Renal Replacement Therapy, Vol. 2, No. 15 (2016) p. 3.

“Chapter 6 – Outpatient Dialysis Services” in “Report to the Congress: Medicare Payment Policy” Medicare Payment Advisory Commission, March 2018, p. 154.

“An Aging Nation: The Older Population in the United States” By Jennifer Ortman et al., U.S. Census Bureau, May 2014, https://www.census.gov/prod/2014pubs/p25-1140.pdf (Accessed 9/2/15), p. 1-2; “US Health Spending Trends by Age and Gender: Selected Years 2002-10” By David Lassman et al., Health Affairs, Vol. 33, No. 5 (May 2014), p. 820; “When I’m 64: How Boomers Will Change Health Care” American Hospital Association, May 2007, http://www.aha.org/content/00-10/070508-boomerreport.pdf (Accessed 7/11/16).

“Dialysis Facility Compare – Complete Dataset” Centers for Medicare and Medicaid Services, July 25, 2018, https://data.medicare.gov/data/archives/dialysis-facility-compare (Accessed 10/23/18).

Medicare Payment Advisory Commission, March 2018, p. 160.

“IBISWorld Industry Report OD4038: Dialysis Centers in the U.S.” By James Crompton, IBISWorld, November 2014, p. 18.

“Chapter 10: Dialysis Providers” in “2016 USRDS Annual Data Report: Volume 2- ESRD in the United States” United States Renal Data System, 2016, https://www.usrds.org/2016/view/v2_10.aspx (Accessed 1/31/17).

“Cost, Quality, and Value: The Changing Political Economy of Dialysis Care” By Jonathan Himmelfarb, Arnold Berns, Lynda Szczech, and Donald Wesson, Journal of the American Society of Nephrology, Vol. 18, No. 7 (2007), p. 2023.

Crompton, November 2014, p. 20.

“Association between Kidney Transplant Center Performance and the Survival Benefit of Transplantation Versus Dialysis” By Jesse D. Schold, et al., Clinical Journal of the American Society of Nephrology, Vol. 9, No. 10 (October 2014) p. 5.

“Transplants in the U.S. by State – Kidney” Organ Procurement and Transplantation Network, September 30, 2018, https://optn.transplant.hrsa.gov/data/view-data-reports/national-data/# (Accessed 10/23/18). CONSULTANT calculated the Compound Annual Growth Rate (CAGR) for the periods indicated to illustrate annual growth of U.S. kidney transplants from 2013 to 2017. CAGR was calculated using the following formula: CAGR = [(New Procedures / Old Procedures) ^ (1 / Years Elapsed)] -1

Medicare Payment Advisory Commission, March 2018.

Crompton, November 2014, p. 20.