Previous issues of Health Capital Topics have discussed several strategies by which healthcare providers and stakeholders have attempted to remain financially viable while combating the rising costs of healthcare, e.g., vertical integration and horizontal consolidation,1 and the market entry of non-traditional providers such as Amazon and Walmart.2 Another, converse strategy – which involves the use of an increasing number of retail clinics and urgent care centers in an effort to provide better point-of-care access to consumers – can help avoid costly and unnecessary visits to a hospital emergency room for conditions such as upper respiratory conditions; ear infections; and, other non-acute conditions.3 Over the last few years, a new type of healthcare provider has entered the market to bridge the gap between these urgent care centers and full service hospitals: the micro-hospital.4 Despite the consolidation trends in the healthcare industry, micro-hospitals have emerged as a popular option for both patients (as they are typically conveniently located, and offer a shorter wait time than traditional hospitals), and providers (due to their relatively small overhead and the ability to bill at hospital rates, in contrast to the lower rates billed by urgent care centers).5 This Health Capital Topics article, the first installment of a five-part series, will introduce the concept of micro-hospitals and briefly discuss how they have evolved within the current healthcare delivery environment. The following articles in this series will further examine micro-hospitals in relation to the Four Pillars that influence the value of entities within the healthcare industry, i.e., regulatory; reimbursement; competition; and, technology.

The term “micro-hospital” is still so new that it cannot be found in the dictionary or in any formal healthcare regulations. As such, the most commonly accepted definition for these entities has been broadly detailed by Emerus, creator of the first micro-hospital prototype, and current operator of more than 28 of these facilities across the U.S.6 The Emerus micro-hospital prototype has the following characteristics:

It is licensed as an independent hospital;

Its size is 30,000 to 60,000 square feet;

It contains 8 emergency beds and staffs board-certified emergency physicians;

It contains 8 to 10 inpatient beds;

It is staffed and open 24 hours per day, 7 days per week;

It maintains transfer agreements with partner hospitals; and,

It provides a core set of ancillary services (which can vary by location), e.g., imaging, surgery centers.

7

Hospitals (with the exception of critical access hospitals [CAH])8 have not historically been subject to specific regulation with regard to size, and hence, a micro-hospital can vary considerably from Emerus’s prototype with regard to number of beds; specific services offered; and, structure. However, as with any newcomer to the healthcare market, micro-hospitals are subject to many of the same trends and market forces that impact other providers. As such, these small facilities may face financial challenges in a market that rewards facilities for taking advantage of economies of scale and scope.9

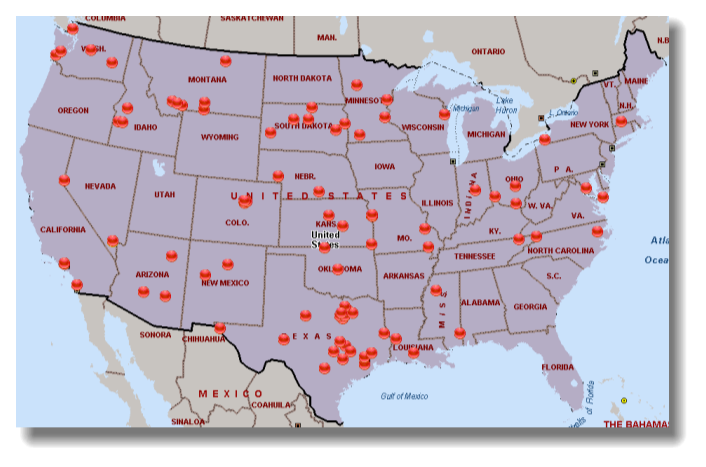

As noted above, Emerus is the premier operator of micro-hospitals in the U.S. with more than 28 currently in operation and more than 20 additional facilities in development.10 Notably, all of Emerus’ functioning micro-hospitals were established in partnership with larger health systems, e.g., Memorial Hermann, Baylor, SCL Health,11 which may allow these systems to utilize new micro-hospitals to expand patient access; better coordinate care; and, promote branding in new communities.12 A representative map of locations for U.S. micro-hospitals (as of April 2018) is shown below.13

The Future for Micro-Hospitals in an Era of Reform

The rapidly shifting sands of healthcare reform over the past several decades, in concert with the continually rising costs of U.S. healthcare, have stimulated many of the trends currently occurring in the healthcare marketplace, e.g., consolidation, integration, and entry of innovative market providers and structures. Among these new innovations is the micro-hospital, which, while still relatively new, appears to be carving out a unique foothold in the marketplace by providing a balance between emergency and inpatient care and maintaining hospital services at the scale of an ambulatory surgical center. This new blended model of inpatient care, while successful in several markets thus far, has unproven longevity within the ever evolving healthcare marketplace. Investors and providers with an interest in pursuing micro-hospital ventures should be well-versed in general U.S. healthcare trends, as well as on the lookout for any new legislation, regulation, or reimbursement changes that may impact micro-hospital development and function. The following articles in this series will provide more detail regarding some of these trends of which savvy potential investors or developers should be cogniziant prior to diving into the waters of one of the latest innovations in U.S. healthcare.

For more information, see “CVS Announces Potential Acquisition of Aetna” Health Capital Topics, Vol. 10, Issue 11 (November 2017), https://www.healthcapital.com/hcc/newsletter/11_17/PDF/CVS.pdf (Accessed 5/8/2018); “Hospitals Form Pharmaceutical Company to Combat Rising Drug Costs” Health Capital Topics, Vol. 11, Issue 3 (March 2018), https://www.healthcapital.com/hcc/newsletter/03_18/PDF/VI.pdf (Accessed 5/8/2018).

For more information, see “Amazon Joint Venture to Create Healthcare Company” Health Capital Topics, Vol. 11, Issue 3 (March 2018), https://www.healthcapital.com/hcc/newsletter/03_18/PDF/AMAZON.pdf (Accessed 5/8/2018); “Capitalism in U.S. Healthcare: The Case of Walmart” Health Capital Topics, Vol. 11, Issue 4 (April 2018), https://www.healthcapital.com/hcc/newsletter/04_18/PDF/WALMART.pdf (Accessed 5/8/2018).

“Retail Clinic Visits Increase Despite Use Lagging Among Individually Insured Americans” Blue Cross Blue Shield, January 18, 2017, https://www.bcbs.com/the-health-of-america/reports/retail-clinic-visits-increase-despite-use-lagging-among-individually?utm_campaign=hoa-retail&utm_content=&utm_medium=release&utm_source=bcbscom (Accessed 4/20/18), p. 1, 4; “Urgent Care Industry White Paper 2018 (Unabridged): The Essential Role of the Urgent Care Center in Population Health” By Laorel Stoimenoff and Nate Newman, Urgent Care Association of America, 2017, p. 4.

“Emerus, The Nation’s Innovator of Micro-Hospitals” Emerus, March 30, 2017, https://www.beckershospitalreview.com/pdfs/EmerusWebinar0317.pdf (Accessed 4/19/18), p. 11.

“Micro-Hospitals: Smaller Facilities with a Big Future” By Kim Slowey, Construction Dive, December 5, 2017, https://www.constructiondive.com/news/micro-hospitals-smaller-facilities-with-a-big-future/512235/ (Accessed 4/20/18); “Exploring the Growing Trend of Micro-Hospitals” By Conner Girdley and Tom Kim, Lancaster Pollard, https://www.lancasterpollard.com/the-capital-issue/exploring-growing-trend-micro-hospitals/ (Accessed 5/17/18).

“About Us” Emerus, 2018, http://www.emerus.com/about/ (Accessed 4/19/18).

Emerus, March 30, 2017, p. 9.

“MLN Booklet: Critical Access Hospital” Centers for Medicare & Medicaid Services, August 2017, https://www.cms.gov/Outreach-and-Education/Medicare-Learning-Network-MLN/MLNProducts/downloads/CritAccessHospfctsht.pdf (Accessed 4/20/18), p. 4.

Slowey, December 5, 2017.

“Locations” Emerus, 2018, http://www.emerus.com/locations/ (Accessed 4/20/18.

Emerus, March 30, 2017, p. 14.

Emerus, 2018; “American Hospital Directory” www.AHD.com, advanced search criteria for hospitals with 1 to 10 beds, not including those listed or identified by keyword as rehabilitation, specialty, surgical or otherwise limited service hospitals (Accessed 4/20/18).