Medicare Advantage (MA) plans, also known as Part C plans, serve as a supplement or an alternative to Original (also called Traditional) fee-for-service (FFS) Medicare Part A and Part B coverage, but they are still part of the Medicare program.1 Most of these plans also include Part D (drug) coverage. MA was created by Congress to offer seniors an alternative to Original Medicare – with an emphasis on treating and managing the health of the whole patient. MA plans are offered to Medicare beneficiaries by Medicare-approved private companies, known as MA Organizations (MAOs), that must follow rules set by Medicare.2

Under the MA program, Medicare purchases insurance coverage for Medicare beneficiaries from private MA plans. These plans can be advantageous for beneficiaries because they limit patient out-of-pocket costs for covered services (although out-of-pocket costs vary by plan) and may cover additional healthcare services (e.g., fitness programs, vision, dental, hearing) as well as other benefits (e.g., transportation to appointments, drugs/services that promote wellness).3 Further, MA plans cannot charge more than Original Medicare for certain services like chemotherapy, dialysis, and skilled nursing facility care.4 However, in order to manage costs, MAOs may require beneficiaries to utilize providers in the plan’s network. Providers can join or leave a plan’s provider network (and the network can change providers) anytime during the year.5

There are a number of different types of MA plans:

-

Health Maintenance Organization (HMO): A type of plan that usually limits coverage to care from physicians who work for or contract with the HMO. It generally does not cover non-emergency out-of-network care. An HMO may require beneficiaries to live or work in its service area to be eligible for coverage. Beneficiaries are required to choose a primary care physician, and must obtain a referral to see a specialist. HMOs often provide integrated care and focus on prevention and wellness.

-

Preferred Provider Organization (PPO): A type of plan where beneficiaries pay less if they use providers in the plan’s network. Beneficiaries can use physicians, hospitals, and providers outside of the network without a referral for an additional cost. Beneficiaries do not have to choose a primary care physician.

-

Private Fee-for-Service (PFFS) Plans: A type of plan where beneficiaries can see any of the providers in the plan’s network. PFFS plans may not cover non-emergency out-of-network. Beneficiaries do not have to choose a primary care physician and do not have to obtain a referral to see a specialist.

-

Special Needs Plans (SNPs): SNPs are limited to beneficiaries with specific diseases or characteristics, because those plans tailor their benefits, provider choices, and drug formularies to meet the specific needs of that patient population. All SNPs must provide drug coverage. The requirement to choose a primary care physician or whether a referral is required to see a specialist differs by plan.

There are two different categories of MA plans – local and regional. Local plans may be any of the types of plans listed above and may serve one or more counties. Regional plans, on the other hand, may only be PPOs and must serve all of a Centers for Medicare & Medicaid Services (CMS)-designated region (there are 26 regions in all), which comprise one or more states.6 Local and regional plans are also paid differently by CMS. Enrollment in Medicare generally has increased, from 39.6 million beneficiaries in 2001 to an estimated 64 million beneficiaries in 2021.7 This number is projected to further increase by approximately 1.5 million beneficiaries per year between 2022 and 2030, resulting in a projected 76 million Medicare enrollees by 2030.8

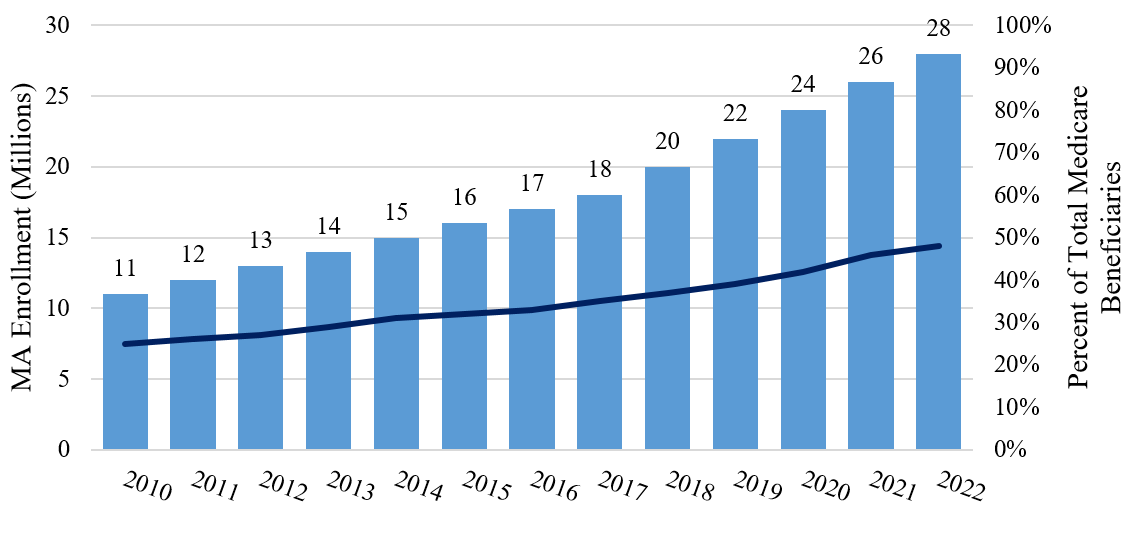

As illustrated in Exhibit 1 below, enrollment in MA plans grew much faster than overall Medicare, more than doubling between 2010 and 2020.9 As of 2022, 28 million Americans were enrolled in an MA plan.10

Medicare Advantage Enrollment, 2010-202211

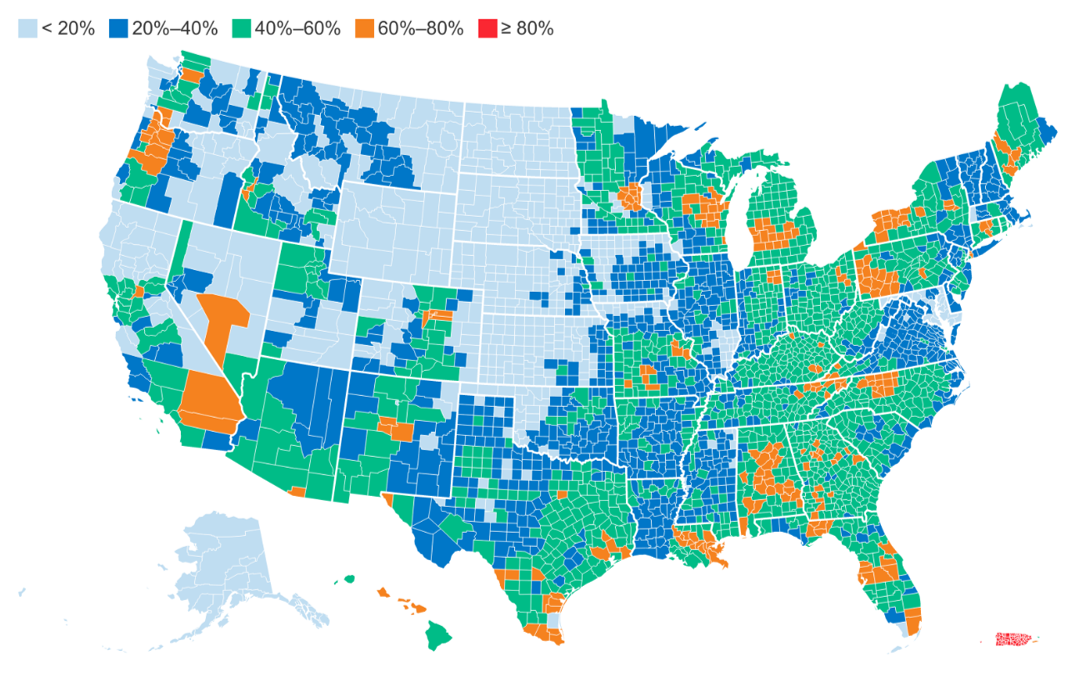

While nearly all Medicare beneficiaries have access to an MA plan,12 it is important to note that MA enrollment is not well-distributed geographically, with the percent of Medicare beneficiaries enrolled in MA highest in the Eastern U.S.

Medicare Advantage Penetration by County, 202213

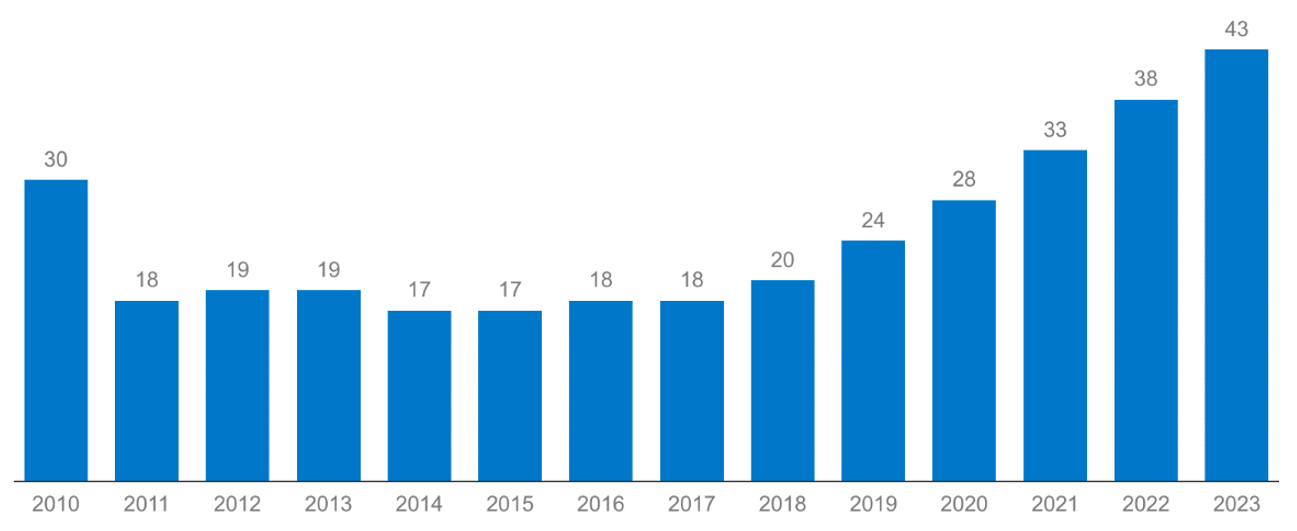

Likely driven by the increasing number of Medicare enrollees, the number of MA plans has increased to 3,998 plans in 2023 (the greatest number of MA plans to date).14 In 2023, the average Medicare beneficiary has access to 43 MA plans (more than double the 2018 number):

Average Number of MA Plans Available to Beneficiaries, 2010-202315

Due to the growing popularity of MA plans, and the number of Americans becoming Medicare eligible every year, MA is still an attractive market for insurers; in 2023, 8 insurers entered the MA market for the first time.16 However, the market is quite concentrated, with UnitedHealthcare and Humana accounting for 46% of the market in 2022.17 Nevertheless, industry experts report that MA competition is continuing to grow, and will have strong momentum going forward.18 This competition is in large part due to the entry of non-traditional plan sponsors such as hospitals and non-healthcare providers. The last few years have seen the emergence of the “payvider,” i.e., health system-sponsored MA plans or MA plans jointly sponsored by payors and providers. In fact, almost 60% of health systems planned to become payviders in 2022.19 Becoming a payvider allows health systems to diversify their risk-based payment strategy and vertically integrate “to gain control over the flow of care and better manage services delivered to members.”20 Additionally, nontraditional healthcare participants, such as Walmart and private equity (PE) firms, are entering the MA market. On September 7, 2022, Walmart and UnitedHealth Group announced a 10-year partnership, wherein jointly-branded MA plans will be offered to seniors in Georgia and Florida, near current Walmart Health locations, eventually expanding across the country to cover hundreds of thousands of beneficiaries.21 This is not Walmart’s first foray into the health plan space – in October 2020, the retail giant announced a partnership with insurer Clover Health to offer MA plans to low-income beneficiaries in Georgia.22 In addition to Walmart, private equity firms have also been entering the MA space; as of 2021, approximately 2% of MAOs were owned by PE firms.23 The entry of these nontraditional players may serve to disrupt the MA space, requiring current MAOs to be nimble in their provision of health services to in order to engage and maintain plan members.

Future installments in this three-part series on the valuation of MA plans will review the reimbursement and regulatory environments in which MA plans operate and the technological advancements being leveraged by MAOs to engage current members and attract new members.

“Medicare Advantage Plans” Medicare.gov, https://www.medicare.gov/sign-upchange-plans/types-of-medicare-health-plans/medicare-advantage-plans (Accessed 3/3/23); “Things to know about Medicare Advantage Plans” Medicare.gov, https://www.medicare.gov/sign-upchange-plans/types-of-medicare-health-plans/things-to-know-about-medicare-advantage-plans (Accessed 10/14/22).

“Medicare Advantage Plans” Medicare.gov, https://www.medicare.gov/sign-upchange-plans/types-of-medicare-health-plans/medicare-advantage-plans (Accessed 3/3/23).

“Things to know about Medicare Advantage Plans” Medicare.gov, https://www.medicare.gov/sign-upchange-plans/types-of-medicare-health-plans/things-to-know-about-medicare-advantage-plans (Accessed 3/3/23).

“Medicare Advantage Program Payment System” Medicare Payment Advisory Commission, Payment Basics, November 2021, p. 1.

“Traditional Medicare” Medicare Data Hub, The Commonwealth Fund, https://www.commonwealthfund.org/medicare-data-hub/traditional-medicare (Accessed 3/3/23).

“Medicare Data Hub” The Commonwealth Fund, October 2020, available at: https://www.commonwealthfund.org/sites/default/files/2020-10/Medicare%20Data%20Hub_October2020.pdf (Accessed 3/3/23), p. 3.

“Medicare Advantage 2023 Spotlight: First Look” Kaiser Family Foundation, November 10, 2022, https://www.kff.org/medicare/issue-brief/medicare-advantage-2023-spotlight-first-look/ (Accessed 3/3/23).

“Medicare Advantage in 2022: Enrollment Update and Key Trends” Kaiser Family Foundation, August 25, 2022, https://www.kff.org/medicare/issue-brief/medicare-advantage-in-2022-enrollment-update-and-key-trends/#:~:text=Medicare%20Advantage%20Penetration%2C%20by%20County%2C%202022&text=In%202022%2C%20one%20in%20five,Advantage%20plans%20(321%20counties. (Accessed 3/3/23).

“Medicare Advantage 2022 Spotlight: First Look” Kaiser Family Foundation, November 2, 2021, https://www.kff.org/medicare/issue-brief/medicare-advantage-2022-spotlight-first-look/ (Accessed 3/3/23).

“Medicare Advantage in 2022: Enrollment Update and Key Trends” Kaiser Family Foundation, August 25, 2022 (Accessed 3/3/23) (based on analysis of CMS Medicare Advantage Enrollment Files, 2022 and March Medicare Enrollment Dashboard, 2022).

“Medicare Advantage 2023 Spotlight: First Look” Kaiser Family Foundation, November 10, 2022, https://www.kff.org/medicare/issue-brief/medicare-advantage-2023-spotlight-first-look/ (Accessed 3/3/23).

“2022 forecast: Medicare Advantage is the industry's hottest market. Don't expect that to change next year” By Paige Minemyer, Fierce Healthcare, December 22, 2021, https://www.fiercehealthcare.com/payer/medicare-advantage-industry-s-hottest-market-2022-don-t-expect-to-change (Accessed 3/3/23).

“Nearly 60% of health systems aim to become 'payviders' in 2022, survey finds” By Robert King, Fierce Healthcare, November 9, 2021, https://www.fiercehealthcare.com/hospitals/nearly-60-health-systems-aim-to-become-payviders-2022-survey-finds (Accessed 3/3/23).

“Walmart And UnitedHealth Group Launch Medicare Advantage Partnership” By Bruce Jaspen, Forbes, September 7, 2022, https://www.forbes.com/sites/brucejapsen/2022/09/07/walmart-and-unitedhealth-group-launch-medicare-advantage-partnership/?sh=6ebaddf84f90 (Accessed 3/3/23).

“Walmart and Clover Health team up to offer Medicare Advantage plans” By Robert King, October 6, 2020, https://www.fiercehealthcare.com/payer/walmart-enters-ma-market-deal-clover-health-to-offer-ga-plans (Accessed 3/3/23).

“Chapter 3: Congressional Request: Private Equity and Medicare” in “Report to the Congress: Medicare and the Health Care Delivery System” Medicare Payment Advisory Commission, June 2021, available at: https://www.medpac.gov/wp-content/uploads/import_data/scrape_files/docs/default-source/default-document-library/jun21_ch3_medpac_report_to_congress_sec.pdf (Accessed 3/3/23), p. 73.